How Home Renovation Loan can Save You Time, Stress, and Money.

Table of ContentsHome Renovation Loan - TruthsNot known Facts About Home Renovation LoanAbout Home Renovation LoanWhat Does Home Renovation Loan Mean?The Definitive Guide for Home Renovation Loan

Many commercial financial institutions supply home renovation loans with marginal documentation requirements (home renovation loan). The disbursal procedure, nevertheless, is made easier if you get the financing from the very same bank where you previously acquired a finance. On the other hand, if you are getting a finance for the very first time, you should repeat all the actions in the funding application procedureConsider a house improvement loan if you desire to restore your residence and provide it a fresh look. With the help of these car loans, you may make your home extra cosmetically pleasing and comfy to live in.

The main benefits of using a HELOC for a home improvement is the flexibility and low prices (usually 1% over the prime rate). In addition, you will only pay interest on the quantity you take out, making this a good option if you need to spend for your home remodellings in phases.

Getting The Home Renovation Loan To Work

The major drawback of a HELOC is that there is no set repayment schedule. You have to pay a minimum of the rate of interest on a monthly basis and this will enhance if prime rates increase." This is an excellent financing option for home remodellings if you intend to make smaller sized monthly repayments.

Offered the possibly long amortization duration, you can finish up paying significantly even more passion with a home mortgage re-finance compared with various other financing options, and the costs related to a HELOC will certainly additionally use. A home loan refinance is successfully a brand-new mortgage, and the rate of interest might be greater than your present one.

Prices and set up costs are normally the very same as would pay for a HELOC and you can repay the financing early without penalty. Some of our consumers will certainly start their renovations with a HELOC and after that switch to a home equity finance as soon as all the costs are confirmed." This can be an excellent home renovation funding alternative for medium-sized jobs.

5 Simple Techniques For Home Renovation Loan

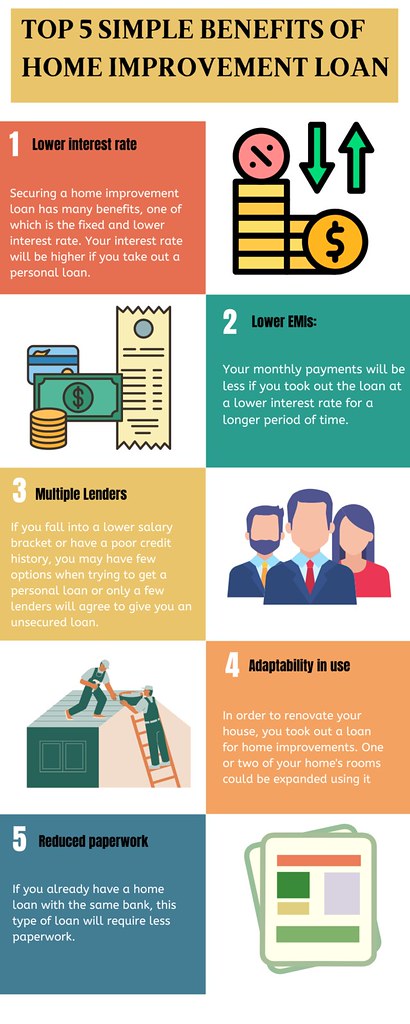

Home improvement fundings are the funding alternative that enables homeowners to remodel their homes without having to dip into their financial savings or splurge on high-interest charge card. There are a variety of home remodelling finance sources available to pick from: Home Equity Credit Line (HELOC) Home Equity Financing Home Loan Refinance Personal Funding Bank Card Each of these funding options comes with distinctive requirements, like useful site credit rating, proprietor's earnings, credit limit, and rate of interest.

Prior to you take the dive of creating your dream home, you most likely would like to know the several sorts of home renovation financings offered in Canada. Below are a few of one of the most common sorts of home renovation loans each with its very own collection of attributes and benefits. It is a sort of home improvement funding that allows home owners to borrow a bountiful amount of cash at a low-interest price.

Home Renovation Loan Things To Know Before You Buy

To be qualified, you need to have either a minimum of at the very least 20% home equity or redirected here if you have a mortgage of 35% home equity for a standalone HELOC. Re-financing your home loan process includes changing your present home mortgage with a new one at a reduced price. It reduces your regular monthly settlements and reduces the amount of interest you pay over your lifetime.

Nevertheless, it is very important to find out the possible threats linked with refinancing your home loan, such as paying a lot more in rate of interest over the life of the lending and costly charges varying from a knockout post 2% to 6% of the loan quantity. Personal fundings are unprotected fundings best suited for those that require to cover home improvement expenditures swiftly however don't have enough equity to get a secured lending.

For this, you may require to supply a clear building and construction plan and budget for the remodelling, including calculating the cost for all the products required. Additionally, personal car loans can be secured or unsafe with shorter payback periods (under 60 months) and featured a higher rates of interest, relying on your credit rating and revenue.

However, for cottage restoration concepts or incidentals that cost a couple of thousand dollars, it can be a suitable option. Furthermore, if you have a cash-back charge card and are waiting on your following paycheck to spend for the deeds, you can make the most of the credit scores card's 21-day poise period, during which no passion is accumulated (home renovation loan).

A Biased View of Home Renovation Loan

Store financing programs, i.e. Installment plan cards are used by lots of home renovation shops in Canada, such as Home Depot or Lowe's. If you're preparing for small home renovation or do it yourself tasks, such as setting up brand-new home windows or washroom renovation, getting a shop card through the retailer can be an easy and fast procedure.

Nonetheless, it is vital to review the conditions of the program very carefully before choosing, as you may be subject to retroactive interest costs if you stop working to repay the equilibrium within the time period, and the rate of interest might be more than regular mortgage funding.